Most people measure their financial success by how much they earn each month—but income alone doesn’t tell the full story. Two people can make the same salary and be in completely different financial positions. That’s where net worth comes in. Your net worth shows what you truly own after subtracting everything you owe, giving you a clear snapshot of your overall financial health.

Understanding how to calculate your net worth is one of the most important steps you can take toward better money management. It helps you see where you stand today, track progress over time, and make smarter decisions about saving, investing, and paying down debt. Whether your number is positive, negative, or somewhere in between, net worth isn’t a judgment—it’s a starting point. In this guide, you’ll learn exactly how to calculate your net worth step by step and how to use it as a practical tool to build long-term financial confidence.

What Is Net Worth? A Clear and Simple Explanation

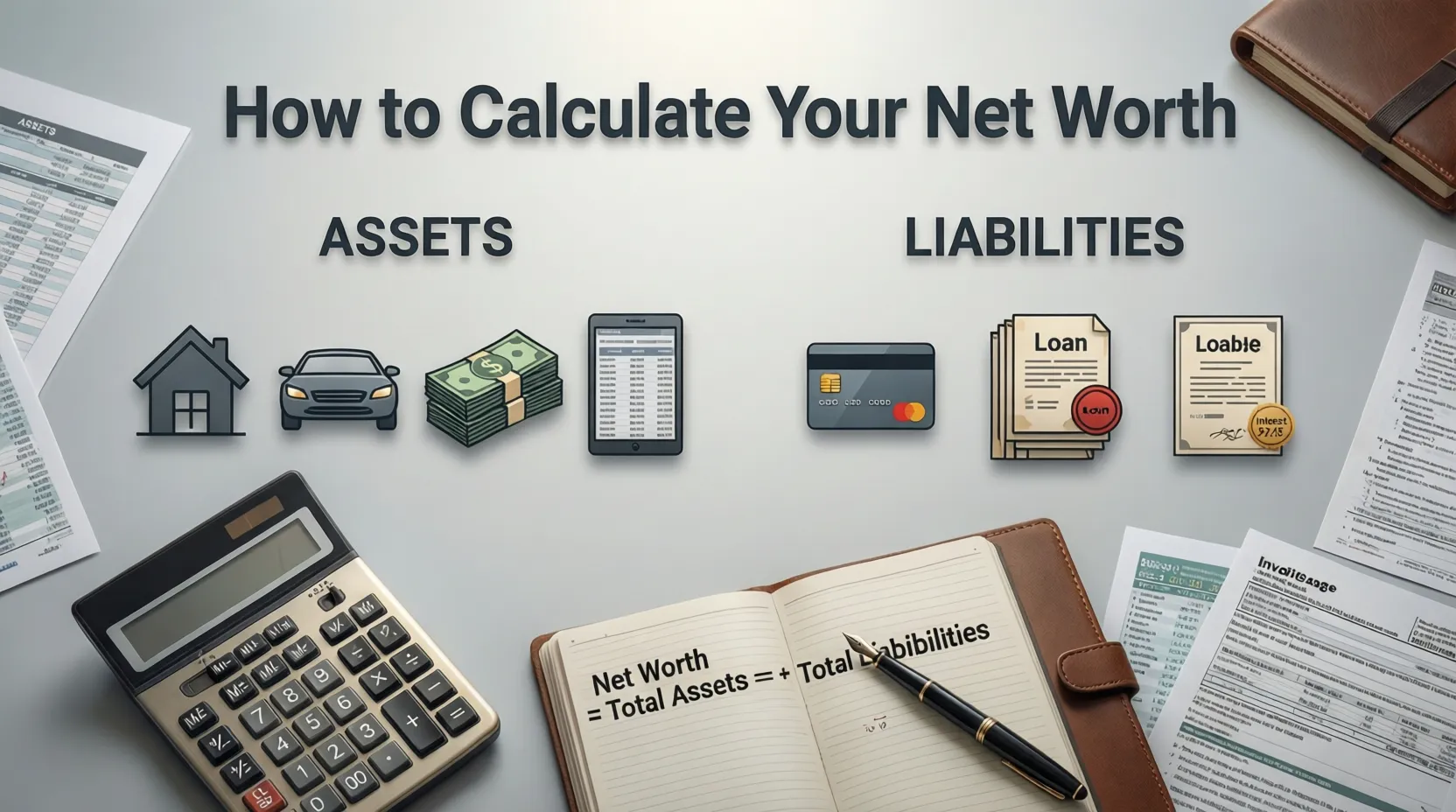

Net worth is a basic but powerful financial concept that represents your overall financial position at a specific point in time. Simply put, your net worth is the difference between what you own (your assets) and what you owe (your liabilities). When you subtract your total liabilities from your total assets, the result is your net worth.

Unlike income, which only shows how much money you earn, net worth provides a more complete picture of your financial health. You might have a high salary, but if you also carry significant debt, your net worth could be low—or even negative. On the other hand, someone with a modest income but low debt and consistent savings may have a strong and growing net worth.

Net worth can be positive, negative, or zero, and all three are common depending on your life stage. For example, students and early-career professionals often have negative net worth due to student loans, while homeowners and long-term investors typically see their net worth increase over time. A negative net worth isn’t a failure—it’s simply a snapshot of where you are right now.

It’s also important to understand that net worth is not permanent. It changes as you pay down debt, save money, invest, or experience major life events like buying a home or starting a business. Think of net worth as a financial dashboard rather than a scorecard. Its real value lies in helping you track progress, identify opportunities for improvement, and make informed decisions that support your long-term financial goals.

The Net Worth Formula (With a Simple Example)

Calculating your net worth follows a straightforward formula, but understanding how it works in practice makes it much more useful. The net worth formula is:

Net Worth = Total Assets − Total Liabilities

Your assets include everything you own that has monetary value, while your liabilities include everything you owe to others. The goal is to determine the total value of each and then subtract one from the other.

For example, imagine you have $15,000 in a savings account, $40,000 in retirement investments, and a car worth $10,000. These assets add up to $65,000. Now, let’s say you also have $20,000 in student loans and $8,000 in credit card debt, for a total of $28,000 in liabilities. Using the formula, your net worth would be $65,000 minus $28,000, which equals $37,000.

This number represents your financial position at that moment in time. If your assets are greater than your liabilities, you have a positive net worth. If your liabilities exceed your assets, your net worth is negative. Neither result is “good” or “bad” on its own—it simply reflects where you currently stand.

What’s important is how this number changes over time. As you pay off debt, increase savings, or invest consistently, your assets grow and your liabilities shrink, improving your net worth. Even small changes—like reducing credit card balances or increasing retirement contributions—can have a meaningful impact. By understanding and using the net worth formula regularly, you gain a clear, measurable way to track your financial progress and stay focused on long-term wealth building.

Step 1: List All Your Assets (What You Own)

The first step in calculating your net worth is identifying and listing all of your assets. Assets are anything you own that has measurable financial value. To get the most accurate picture, it’s important to be thorough and realistic when valuing them.

Start with cash and cash equivalents. This includes checking accounts, savings accounts, money market accounts, and any physical cash you may have. These are typically the easiest assets to value because their worth is clear and up to date.

Next, list your investments. This category includes brokerage accounts, stocks, bonds, mutual funds, exchange-traded funds (ETFs), and cryptocurrency. Use current market values rather than what you originally invested. For volatile assets like crypto, it’s best to use a conservative, current price.

Don’t forget retirement accounts, such as a 401(k), IRA, Roth IRA, or pension accounts. Even though these funds may not be accessible immediately, they are still part of your net worth because they belong to you.

Real estate is another major asset category. Include your primary residence, rental properties, or land, and estimate their current market value based on recent sales or online valuation tools. You can also include vehicles, such as cars or motorcycles, using their current resale value—not what you paid for them.

Finally, consider other valuable assets like business ownership, collectibles, or high-value personal property. If an item would realistically be difficult to sell or has little resale value, it’s usually best to exclude it. The goal is accuracy, not inflation.

Step 2: List All Your Liabilities (What You Owe)

Once you’ve listed your assets, the next step is to identify all of your liabilities—the debts and financial obligations you’re responsible for. Liabilities reduce your net worth, so it’s important to include everything you owe, even balances that may feel small or temporary.

Start with short-term liabilities, which are typically debts that can fluctuate month to month. These include credit card balances, personal loans, buy-now-pay-later plans, unpaid medical bills, and any outstanding balances due within the next year. Use the current balance, not the minimum payment or original amount borrowed.

Next, move on to long-term liabilities. This category usually includes larger debts such as student loans, auto loans, mortgages, and business loans. For each, record the remaining balance—not the original loan amount. If you have multiple loans of the same type, list each one separately for clarity.

Be sure to include other financial obligations that are often overlooked. These may include tax debt, lines of credit, co-signed loans (even if someone else is making the payments), and legal or settlement obligations. If you’re legally responsible for the debt, it should be counted as a liability.

When listing liabilities, accuracy matters more than perfection. Avoid rounding down balances or ignoring inconvenient debts. Seeing the full picture can feel uncomfortable at first, but it provides valuable insight into where your money is going and which debts may be holding back your financial progress. By clearly identifying your liabilities, you create a solid foundation for calculating your net worth and making informed decisions about debt reduction and long-term financial planning.

Step 3: Calculate Your Net Worth and Understand the Result

After listing all your assets and liabilities, calculating your net worth is straightforward. Add up the total value of your assets, then add up the total value of your liabilities. Subtract your liabilities from your assets to arrive at your net worth figure. This single number represents your overall financial position at a specific moment in time.

Once you have your result, it’s important to understand what it means. A positive net worth indicates that you own more than you owe, which is generally a sign of financial stability. A negative net worth means your debts exceed your assets, a situation that’s common early in adulthood or during major life transitions such as starting a business or purchasing a home. A net worth of zero simply means your assets and liabilities are equal.

Regardless of the outcome, your net worth should be viewed objectively. It’s not a measure of success or failure—it’s a baseline. Many people feel surprised or discouraged by their first calculation, but the real value lies in awareness. Once you know your number, you can begin making intentional decisions to improve it over time.

It’s also helpful to recognize that net worth naturally fluctuates. Market changes, debt payments, large purchases, or life events can all cause your net worth to rise or fall. For this reason, comparing your net worth to others can be misleading. Everyone’s financial journey is different.

Instead of focusing on the absolute number, pay attention to the trend. An upward trend over months or years—no matter how gradual—signals progress. Tracking your net worth consistently helps you stay focused, motivated, and aligned with your long-term financial goals.

Common Mistakes to Avoid When Calculating Your Net Worth

While calculating your net worth is conceptually simple, there are several common mistakes that can distort the results and reduce its usefulness. Avoiding these pitfalls will help ensure your net worth accurately reflects your true financial situation.

One of the most frequent mistakes is overestimating asset values. It’s easy to list what you paid for an asset rather than what it’s actually worth today. Homes, vehicles, and personal property should be valued at their current market or resale value—not emotional or purchase price. Overvaluing assets can create a misleading sense of financial security.

Another common error is forgetting certain liabilities. Small debts, such as store credit cards, buy-now-pay-later balances, or co-signed loans, are often overlooked. Even if the balance feels insignificant, it still impacts your net worth and should be included.

Some people also mistakenly include future income or expected bonuses as assets. Net worth is based only on what you currently own, not what you plan to earn. Similarly, including assets that are difficult or unrealistic to sell—like everyday household items—can inflate your numbers without providing meaningful insight.

Comparing your net worth to others is another trap. Benchmarks and averages can provide context, but they don’t account for differences in age, location, lifestyle, or personal goals. Comparison often leads to unnecessary stress rather than productive action.

Finally, calculating net worth once and never revisiting it limits its value. Net worth is most powerful when tracked over time. By avoiding these mistakes and approaching the process with honesty and consistency, you can use net worth as a reliable tool to guide better financial decisions and long-term wealth building.

How Often Should You Calculate Your Net Worth?

Calculating your net worth once is helpful, but tracking it regularly is what turns it into a powerful financial tool. How often you should calculate your net worth depends on your financial situation, goals, and tolerance for short-term fluctuations.

For most people, quarterly updates strike the right balance. Reviewing your net worth every three months allows enough time to see meaningful changes without becoming overly focused on small ups and downs. Quarterly tracking works well if you’re paying down debt, building savings, or investing consistently.

Some people prefer monthly tracking, especially if they are aggressively working toward financial goals such as debt elimination or saving for a major purchase. Monthly updates can increase awareness and motivation, but they may also reflect market volatility rather than real progress, particularly if you invest heavily.

An annual calculation may be sufficient for those with stable finances, minimal debt, or long-term investment strategies. While less frequent, yearly tracking still provides valuable insight into overall trends and long-term growth.

No matter how often you calculate your net worth, consistency is key. Try to update it on the same date or at the same time each period to keep comparisons accurate. For example, checking at the end of each quarter avoids distortions caused by timing differences.

It’s also important not to obsess over short-term changes. Market fluctuations, large purchases, or temporary expenses can cause your net worth to dip, even if your long-term trajectory is positive. Focus on the trend rather than the exact number.

By reviewing your net worth at regular intervals, you create a clear feedback loop that helps you adjust spending, saving, and investing decisions—keeping you aligned with your long-term financial goals.

Tools and Methods to Calculate Your Net Worth

There are several ways to calculate your net worth, and the best method depends on how hands-on you want to be and how complex your finances are. The key is choosing a system you’ll actually use consistently.

A manual spreadsheet is one of the most popular and flexible options. You can create your own spreadsheet or use a downloadable net worth template to list assets and liabilities in detail. Spreadsheets give you full control, allow customization, and make it easy to track changes over time. The downside is that they require regular manual updates.

Another option is using online net worth calculators. These tools guide you through the process step by step and often provide instant results. They are convenient and beginner-friendly, but many require you to manually enter data each time and may not save your history unless you create an account.

For a more automated approach, financial tracking apps can link directly to your bank accounts, investment accounts, and loans. These tools update your net worth automatically and allow you to see trends in real time. While convenient, automation comes with trade-offs. Account linking may raise privacy concerns, and automated values may occasionally be inaccurate, especially for real estate or business assets.

Regardless of the method you choose, accuracy and consistency matter more than sophistication. Use current values, review entries periodically, and adjust for changes such as loan paydowns or investment growth.

Many people find success combining methods—using automation for everyday accounts and a spreadsheet for higher-level tracking. The best tool is the one that helps you clearly understand your financial position and supports informed, confident decision-making over time.

How to Improve and Grow Your Net Worth Over Time

Once you know your net worth, the next step is using it as a guide to improve your financial future. Growing your net worth comes down to two core actions: increasing assets and reducing liabilities. Making steady progress in both areas creates long-term financial momentum.

One of the most effective ways to increase assets is by consistently saving and investing. Building an emergency fund protects you from relying on debt, while investing—especially through retirement accounts—allows your money to grow through compound interest. Even small, regular contributions can make a significant difference over time.

Increasing your earning potential also plays an important role. This may include advancing your career, learning new skills, negotiating your salary, or building additional income streams. While higher income doesn’t automatically increase net worth, it creates more opportunities to save, invest, and pay down debt when managed intentionally.

On the liability side, focus on reducing high-interest debt first. Credit cards and personal loans can significantly slow net worth growth due to interest costs. Creating a structured debt payoff plan—such as the snowball or avalanche method—can accelerate progress and free up cash for asset-building.

It’s also important to avoid lifestyle inflation. As income increases, keeping expenses in check allows more money to flow toward financial goals rather than consumption.

Improving net worth is rarely about dramatic changes. Instead, it’s the result of consistent habits practiced over time. By tracking your net worth regularly and making small, intentional adjustments, you create a clear path toward long-term financial stability and confidence.

Final Thoughts

Your net worth is one of the most useful financial metrics you can track—but only if you view it the right way. It’s not a measure of personal success, intelligence, or worth. Instead, it’s a practical tool designed to help you understand where you stand financially and make better decisions moving forward.

It’s completely normal for your net worth to fluctuate over time. Market movements, major purchases, debt paydowns, and life events can all cause short-term changes. What matters most is the long-term direction. An upward trend—even a slow one—signals progress and healthy financial habits.

Rather than comparing your net worth to others or chasing arbitrary benchmarks, focus on what the number tells you about your own situation. Are your debts shrinking? Are your assets growing? Are you moving closer to your personal financial goals? These insights are far more valuable than the number itself.

Net worth is especially powerful when paired with action. Use it to identify opportunities to save more, reduce debt, or invest more effectively. Revisit it regularly, adjust your strategy as needed, and celebrate progress along the way.

Ultimately, calculating your net worth is about clarity and control. When you understand your full financial picture, you’re better equipped to plan, adapt, and make confident choices with your money. Start where you are, stay consistent, and let your net worth guide you—not define you—on your journey toward long-term financial well-being.

{kind=link}